A decade ago, before the Brexit referendum, economists trying to work out the economic consequences of the United Kingdom leaving the European Union had to do a lot of guess work. Economic history does not have many examples of a major advanced economy choosing to exit from a deep trading arrangement with its neighbours.

Some people turned to the break-up of the Soviet Union as an analogy, while others examined Czechoslovakia’s “velvet divorce” of 1992. None of the examples quite fit, so there was a heavy reliance on theory and models.

Ten years later, economists can at least be thankful to British voters, and to the politicians who oversaw the process of withdrawal, for providing them with a real-world case study. The simple intuition, which did not require an especially advanced education in economics, that putting up trade barriers with your largest trading partner will result in less trade and less growth turns out to be correct. While the process was not pleasant for the British people, a useful experiment has been conducted.

A major study of the costs of Brexit, published by the US National Bureau of Economic Research last year, looked back at the initial projections of economists from 2015 and 2016 and compared them with what has actually played out. Of course nothing in macroeconomics is ever entirely straightforward. The pandemic and its lockdowns, the impact of the wars in Ukraine and Iran and the resulting spike in energy prices, complicate any analysis.

Suggested Reading

The Brexiteers all in a pickle over Monster Munch

But in general the authors of the study felt confident to argue that estimates made in 2016 were broadly accurate over a five year period but had underestimated the costs of Brexit after a decade. They found that, relative to a counterfactual of no Brexit, Britain’s national income – its GDP – had been reduced by around six to eight percentage points. That is, even in macroeconomic terms, a big number.

Those costs came about in various ways, at different times over the last decade and started the day after the referendum itself – well before Britain actually left the EU.

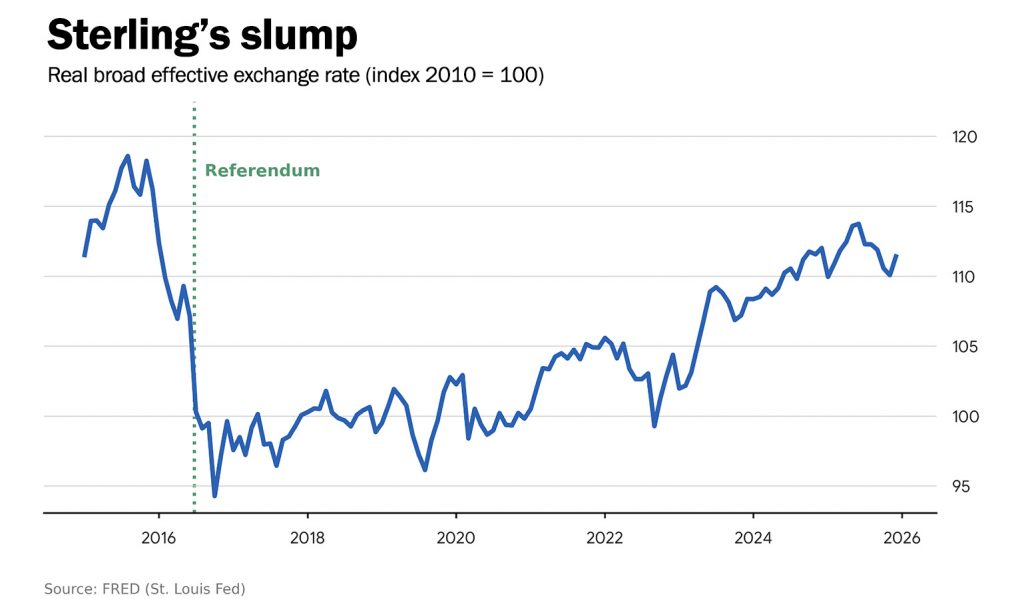

The first casualty was sterling

As the results became clear, in the early hours of the 23rd of June 2016, the pound began a deep nosedive in Asian trading. In the course of that day, sterling fell around 10% against the dollar and 7% against the euro – the largest one day falls since the collapse of Lehman Brothers. Against the dollar, the pound slumped to its lowest level since 1985.

The chart gives the value of sterling weighted against a range of other currencies, and shows that the sterling slump continued until the autumn of 2016. The pound then remained near its lows all the way into the early 2020s.

The pound effectively acted as the first shock absorber, as foreign holders of UK assets sought to cut their exposure to the UK following an unexpected decision by the electorate. And with the fall came costs, felt by the British people in the form of higher prices.

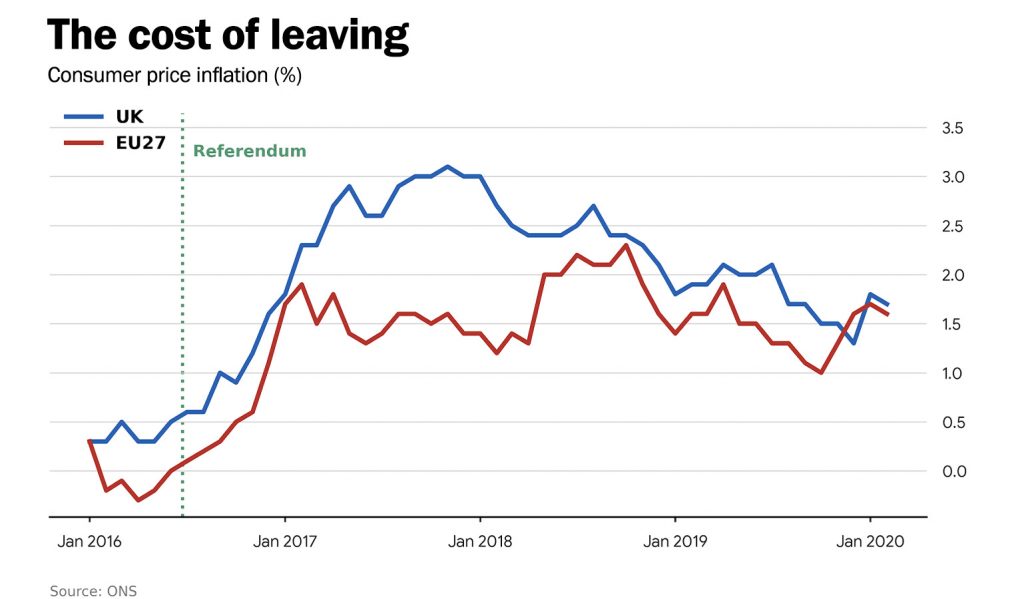

While a weaker pound may provide some support for British exporters, making their wares effectively cheaper overseas, it also directly raises the prices of imported goods. A simple comparison of British and EU inflation over the period captures the impact (see chart).

In June 2016, British inflation was rising at an annual pace of 0.5% and inflation across the EU-27 (excluding the UK) was actually at zero, the gap was 0.5%. One year later while EU inflation had ticked up to an annual rate of 1.3%, consumer price inflation in the UK was running at 2.6% – a gap of 1.3%.

Much of that widening gap, which would remain elevated until mid-2018 by which point sterling had stabilised at a lower level, reflected what was happening in the foreign exchange markets. Brexit rattled investors, they dumped the pound and the long squeeze on the real incomes of British workers was prolonged.

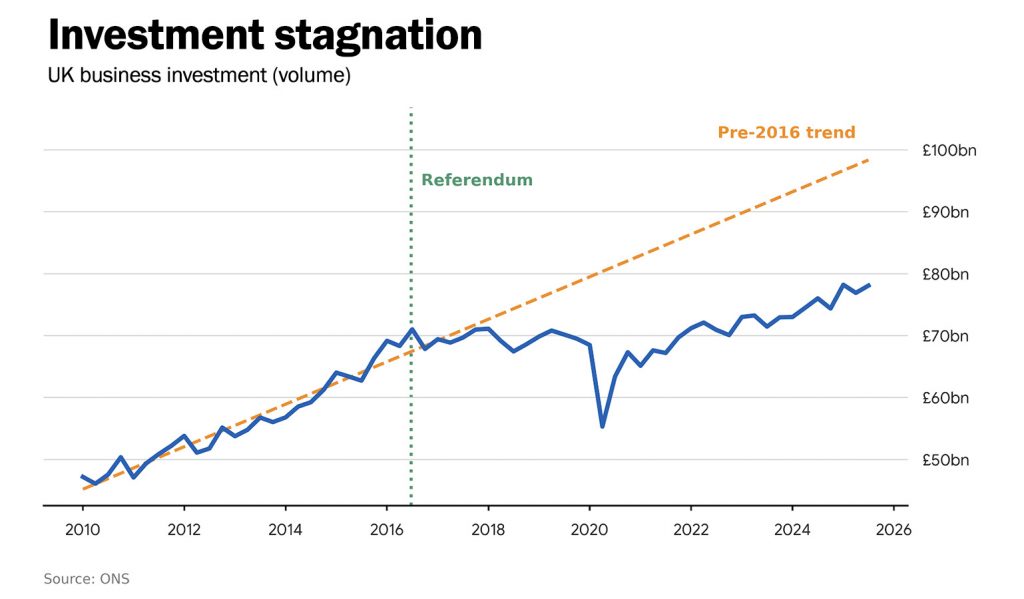

Vanishing business

The second major pre-withdrawal impact of Brexit was more visible in business investment. The immediate problem facing the managers of firms in the summer of 2016 was that the British people had voted to leave the European Union but no one quite knew exactly what that meant in practice. Even relatively straightforward questions, such as “when would Article 50 actually be triggered?” – the clause of the Treaty that would begin the two year countdown to exit – were open to debate.

The details of the eventual endgame dominated British politics, and British political coverage, for years. The questions included: whether the UK would remain in the single market; whether it would leave the customs union; whether there would be any trade deal with the EU, or whether Britain would simply trade with the continent on World Trade Organisation terms.

There was a large rise in economic uncertainty and uncertainty has a big effect on economic performance. In the face of elevated uncertainty, firms tend to hold off on investment decisions and even occasionally pause hiring. In the case of Brexit, this was understandable. Britain’s future trading relationship with the EU was completely up in the air.

Business investment which had been on a steady upward path since 2010, as part of a gradual recovery from the crisis of 2008-09, essentially flat-lined in the second half of the 2010s (see chart). That both had an immediate impact on growth in the short term, by reducing business spending and hence overall demand in the economy and almost certainly a lasting impact on productivity growth in the future.

All things being equal, to use an economist’s favourite phrase, higher investment should mean greater output per worker, and a half decade of lost business investment will mean lower output worker in the future. What is more, much of this “missing” investment ended up not being paused but cancelled. There was no sudden burst of “catch-up” investment once uncertainty diminished and it became clear Britain was heading for a “hard” Brexit.

According to a survey of British executives conducted by the Bank of England, the most commonly paused or cancelled types of investment were in machinery and equipment. Software budgets, training budgets and research and development budgets all also felt the pinch.

High uncertainty over the eventual shape of Brexit did not only push down on business investment. It also consumed a great deal of management time. The Decision Maker Panel data, collated by the Bank of England, suggests that between 2017 and 2020 three quarters of British Chief Financial Officers (CFOs) had to spend time every week making Brexit preparations and for a quarter of them this consumed between one and five hours each week.

For an unlucky 10%, presumably in especially EU-exposed sectors, Brexit preparations consumed an average of slightly more than six hours a week, which depressed productivity. And while the evidence of the damage down to firms by all that Brexit preparation, there was an even larger – and harder to quantify – impact on the civil service and political leaders.

Alongside the impact of weaker sterling and higher inflation, flat-lining investment and management distraction, the years between 2016 and early 2020 also saw depressed consumer confidence. Also, many firms were forced to bear the costs of building up additional stockpiles, as the reliability of supplies from the EU was placed in doubt.

Suggested Reading

Sadiq Khan speaks the Brexit truth the nation needs to hear

And all of this happened before Britain had actually left the European Union. The absence of a clearly agreed plan and the high level of political turmoil (a messy – and arguably unnecessary – 2017 general election together with frequent changes of Prime Minister) meant that uncertainty was much higher than it had to be.

While many of the costs of Brexit were unavoidable, it is also true that had a clear outline of Brexit been in place by, say, 2017 or 2018, then the immediate economic damage could have been lessened. But there was no plan. The damage was enormous.

Trade

The second major set of economic consequences came once the UK had actually left the EU. The largest impact here was to trade. This is where the economics become simple – if a country puts new trade frictions into a previously almost frictionless trading relationship, then there will be less trade as a result. And when the trading relationship in question is your largest trading relationship, the damage is magnified.

The impact of Brexit on Britain’s imports and exports is something that can only ever be estimated rather than measured. We simply do not know what those figures would look like in the absence of the referendum. And of course, the impacts of the pandemic and the energy price shock of 2021-23 cloud the picture. The exports of pretty much every country fell in 2020 and rebounded afterwards.

Perhaps the cleanest measure is to look at export growth in the UK and compare it to what happened in peer economies. Between 2019 and 2024 British exports grew at an annualised pace of under 0.5%, while those of Germany and France grew around twice as quickly, those of Japan grew three times as fast and those of America at four times the pace.

Another way to look at similar issues is to measure the trade intensity of GDP, that is to say if one totals up imports and exports and asks how much of a share, they are together of total national income. This is a standard measure of how open an economy is to the rest of the world.

As one might expect, the trade intensities of all major economies fell sharply in 2020 as lockdowns disrupted cross-border trade. The UK’s trade intensity, by the end of 2024, was roughly back to pre-pandemic levels. By contrast the trade intensity of the European Union was about 10% higher than early 2020 by then and that of the rest of the G7 group of advanced countries (excluding the UK) was up by a similar amount.

One can argue whether exports or trade intensity are the better measure and question whether the right comparator is France, Germany, Japan, the United States, the G7 or the EU. But whichever measure you prefer, the implication is the same: Britain’s trade and exports have lagged her peers since Brexit took effect.

In the long run the Office of Budget Responsibility, Britain’s official forecaster, believes that Brexit will result in the country’s imports and exports being around 15% lower than they otherwise would have been. Notably that analysis includes the impacts of supposed Brexit wins from the UK having the freedom to set its own trade policy. Trade deals with India, Australia and so on are simply not enough to turn the dial back the other way.

The big economic hit though does not come directly from those weaker exports and weaker imports but from the knock-on effect of lower trade on productivity. Less trade means less competition and less competition means, in the longer run, lower productivity.

With less access to the European markets, there is less scope for successful British exporters to grow their revenues and expand. And with less competition from European firms, there is more chance that weak British businesses, in sectors which import from the EU, can stagger on for longer. More generally a smaller overall market allows for less specialising in areas of comparative advantage.

In the broad sweep of post-War British economic history the 1950s and 1960s saw a decline in trade intensity as governments sought to shelter British industry from foreign pressure. The result was weak productivity growth and a long period of relative economic decline.

After the UK entered what was then the European Economic Community in 1973, trade intensity began to rise and productivity began to grow faster. Of course the effects took time to show up in the data but a strong case can be made that this opening up to competitive pressure was at least as large, if not a larger, factor in Britain’s stronger performance in the 1980s and 1990s than any of the changes implemented by Maragaret Thacher’s governments.

An economy that turns inward is generally one where growth will be weaker in the long-run and Brexit represents the single largest voluntary inward turn ever performed by an advanced economy.

The OBR reckon the long-term hit to GDP is worth around 4% of national income, others – as noted – go for larger figures of 6-8%. Either way the number is big.

Neither estimate should be taken as an argument that the UK rejoining the EU – or the single market or customs union – would suddenly, or even ever, boost GDP back to where it would have been if Britain had voted to remain. Real economic harm has been done that may not be repairable. If you drive your car into a bollard, reversing away does not undo the damage.

On the other hand, continuing to accelerate will result in an even larger repair bill for your vehicle. The best estimates do all suggest that rejoining the single market, rejoining the customs union, agreeing to a deeper trading relationship with the EU – or even rejoining – would all result in economic gains. At first through higher exports and imports and, eventually, through the workings of more competitive pressure driving productivity growth higher.

It’s getting worse

Britain’s economy was not in great shape in mid-2016. There were reasons after all, however misplaced, why people voted for Brexit. A decade on though, the mess has clearly become worse. Whether one prefers the higher or the lower estimates of the total costs, they remain substantial – far larger than those of any other major policy decision in the last few decades in economic terms. The longer Britain’s trade intensity remains below where it could be, the greater the damage that will be done.

The Brexit experiment then has been something of a boon for macroeconomists. The next time a country considers severing a deep trading relationship, there will at least be an empirical example to point to. The appetite for leaving the EU does seem to have fallen across the continent, even among the eurosceptic hard-right parties.

The real losers though have been the British people, who have suffered even at the cost of advancing economic understanding. The gains in wider knowledge never outweigh the costs for the lab rats involved.

Most popular

Most popular

Screen scandal: How Ofcom lets GB News get away with it

GB News Scandal: Read our dossier of their flagrant Ofcom breaches

GB News Scandal: The presenters

Claudia Winkleman’s chat show is afraid of Claudia Winkleman